The other day I was having a conversation with a friend of mine about the benefits and shortcomings of two very different retirement programs. His argument was that a tax-deferred program would give you the best options for growth and tax advantages. My argument was against this "traditional" thinking by suggesting that an income tax free program, a program which is funded with post tax money, would be better. After much debate, I finally ran the numbers. You will see below what they reveal...

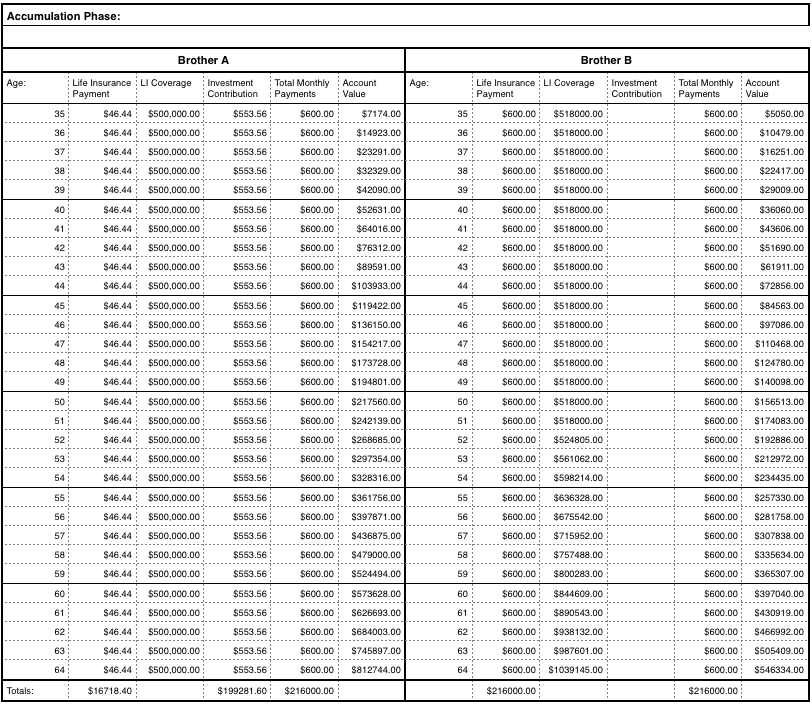

Illustration Assumptions:

-Each brother is a healthy 35yr old male looking to retire at age 65.

-Each brother has $600/mo. to budget for life insurance and retirement savings, for 30yrs.

-Both brothers have roughly $500,000 life insurance, Brother B has ($518,000).

-Both brothers are earning an assumed 8% return on their programs. (Real world results could, and most likely would, vary).

-Brother A is choosing to "buy term and invest the difference". This is a strongly recommended strategy by many financial professionals. (I used the Retirement Income Calculator from BankRate.com to provide the figures shown. For the life insurance quote I used illustration software that I have).

-Brother B is using a life insurance program to accumulate cash value. (Yes, I said life insurance to save money... more on that later. The figures are taken from an illustration I ran in the life insurance software).

Illustration Assumptions:

-Each brother is a healthy 35yr old male looking to retire at age 65.

-Each brother has $600/mo. to budget for life insurance and retirement savings, for 30yrs.

-Both brothers have roughly $500,000 life insurance, Brother B has ($518,000).

-Both brothers are earning an assumed 8% return on their programs. (Real world results could, and most likely would, vary).

-Brother A is choosing to "buy term and invest the difference". This is a strongly recommended strategy by many financial professionals. (I used the Retirement Income Calculator from BankRate.com to provide the figures shown. For the life insurance quote I used illustration software that I have).

-Brother B is using a life insurance program to accumulate cash value. (Yes, I said life insurance to save money... more on that later. The figures are taken from an illustration I ran in the life insurance software).

At the end of the accumulation phase it would appear that Brother A is in a much better program. He has accumulated an illustrated $812,744 vs. Brother B's $546,334. However, as I remind people on a regular basis, retirement is about INCOME, not the lump sum you start with.

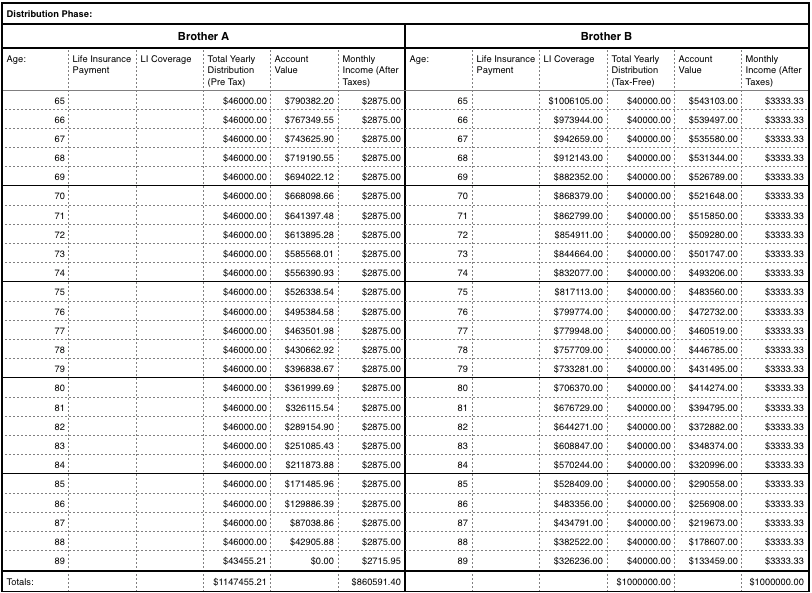

See what happens during the distribution phase:

Brother A, at retirement, chooses to place his accumulated nest egg in a program earning 4% interest while providing protection against market volatility. Moving money into a safe, guaranteed program is publicly considered a smart idea. For the sake of this illustration we are assuming that he will be paying a 25% rate of taxes on his income.

Brother B, however, continues to earn 8% on his account value because there is no need to make any changes due to risk (There is no risk to accumulated values due to market volatility), and because the money is using a life insurance program, there are no taxes on the distributions as long as the program stays in-force.

Each brother is illustrated to withdraw money until the end of age 89.

Brother A has no life insurance at this time because the 30yr Term Life Insurance program has expired.

Brother B starts the Distribution Phase with over $1M death benefit (decreasing as he withdraws money from the program).

See what happens during the distribution phase:

Brother A, at retirement, chooses to place his accumulated nest egg in a program earning 4% interest while providing protection against market volatility. Moving money into a safe, guaranteed program is publicly considered a smart idea. For the sake of this illustration we are assuming that he will be paying a 25% rate of taxes on his income.

Brother B, however, continues to earn 8% on his account value because there is no need to make any changes due to risk (There is no risk to accumulated values due to market volatility), and because the money is using a life insurance program, there are no taxes on the distributions as long as the program stays in-force.

Each brother is illustrated to withdraw money until the end of age 89.

Brother A has no life insurance at this time because the 30yr Term Life Insurance program has expired.

Brother B starts the Distribution Phase with over $1M death benefit (decreasing as he withdraws money from the program).

Results:

While Brother A is pulling out more money in retirement ($46,000 vs. $40,000), he has to pay taxes on his income. His after tax income falls short of Brother B.

After 25yrs of income, Brother A has run out of money and has no life insurance. Brother B has pulled out $1M Tax-Free income from his plan, has over $300k life insurance and still $133,459 account value.

Now, I'm not here to tell you which program is best for you. That's for you to speak with your financial professional and determine for yourself. However, for the sake of argument, I believe I've won.

Have anything to add? Please comment below!

After 25yrs of income, Brother A has run out of money and has no life insurance. Brother B has pulled out $1M Tax-Free income from his plan, has over $300k life insurance and still $133,459 account value.

Now, I'm not here to tell you which program is best for you. That's for you to speak with your financial professional and determine for yourself. However, for the sake of argument, I believe I've won.

Have anything to add? Please comment below!

Zack Hurst is a Licensed Insurance Professional, not a certified public accountant, tax advisor or financial planner. The information provided above is not meant to be advice for any specific person or scenario. The illustrative comparison provided is only meant for informational purposes only. Consult your personal financial professional with any questions related to your own retirement goals.

RSS Feed

RSS Feed